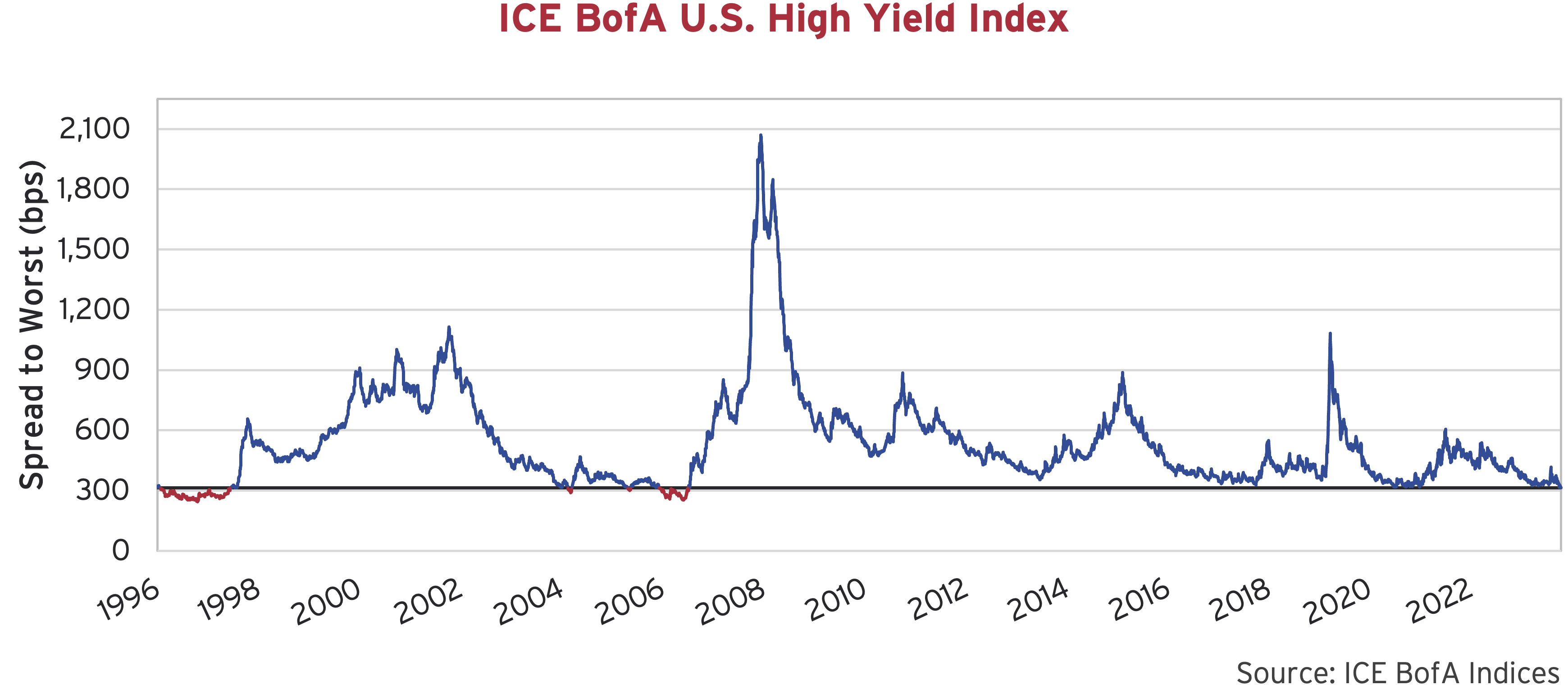

Come On In

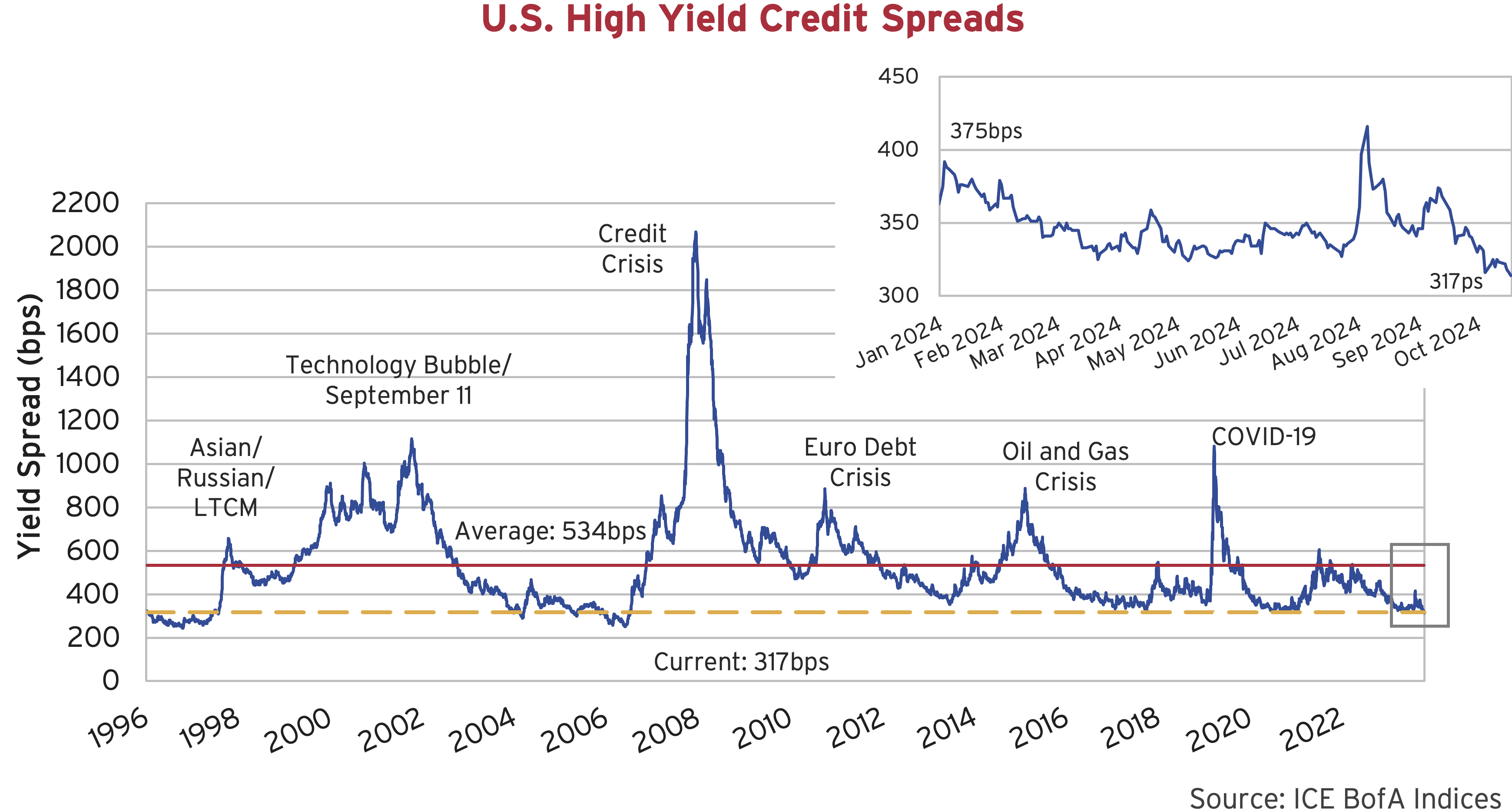

Another quarter has passed, and we continue to watch corporate credit spreads “Come On In”. Despite significant volatility over the August long-weekend, high yield spreads ended the quarter tighter than where they began. The “Spread to Worst” on the ICE BofA U.S. High Yield Index touched 313 basis points (bps) on October 21st, a level not seen since the eve of the Great Financial Crisis. We can see from the red in the chart below that we are indeed in rare territory.

The Water’s Fine

The 2022-2024 monetary tightening chapter officially came to a close on September 18th when Jerome Powell and the Federal Open Market Committee voted to lower the target range for the federal funds rate by 50 bps. Inflation continues its move towards 2% in the U.S. and job gains have moderated. Judging this, the Federal Reserve and bond investors seem to be in agreement that everything is under control.

Closer to home, the Bank of Canada (BOC) implemented its fourth consecutive cut in October, this time a 50 bps reduction, bringing the overnight rate down to 3.75%. Inflation has been cooling much more quickly in Canada relative to the U.S. as higher interest rates have a more direct impact on our real estate and financial services heavy economy. In a surprise release that caught even industry insiders off-guard, the Federal Liberals announced that they would be increasing the cap on mortgage insurance from $1.0 to $1.5 million and extending amortizations out to 30 years. This, in an effort to “make mortgages more affordable” and kickstart an ailing industry. It is no secret that we have a housing affordability crisis in this country following many years of binging on cheap mortgage debt. In our view, the answer to too much debt is not “more debt”.

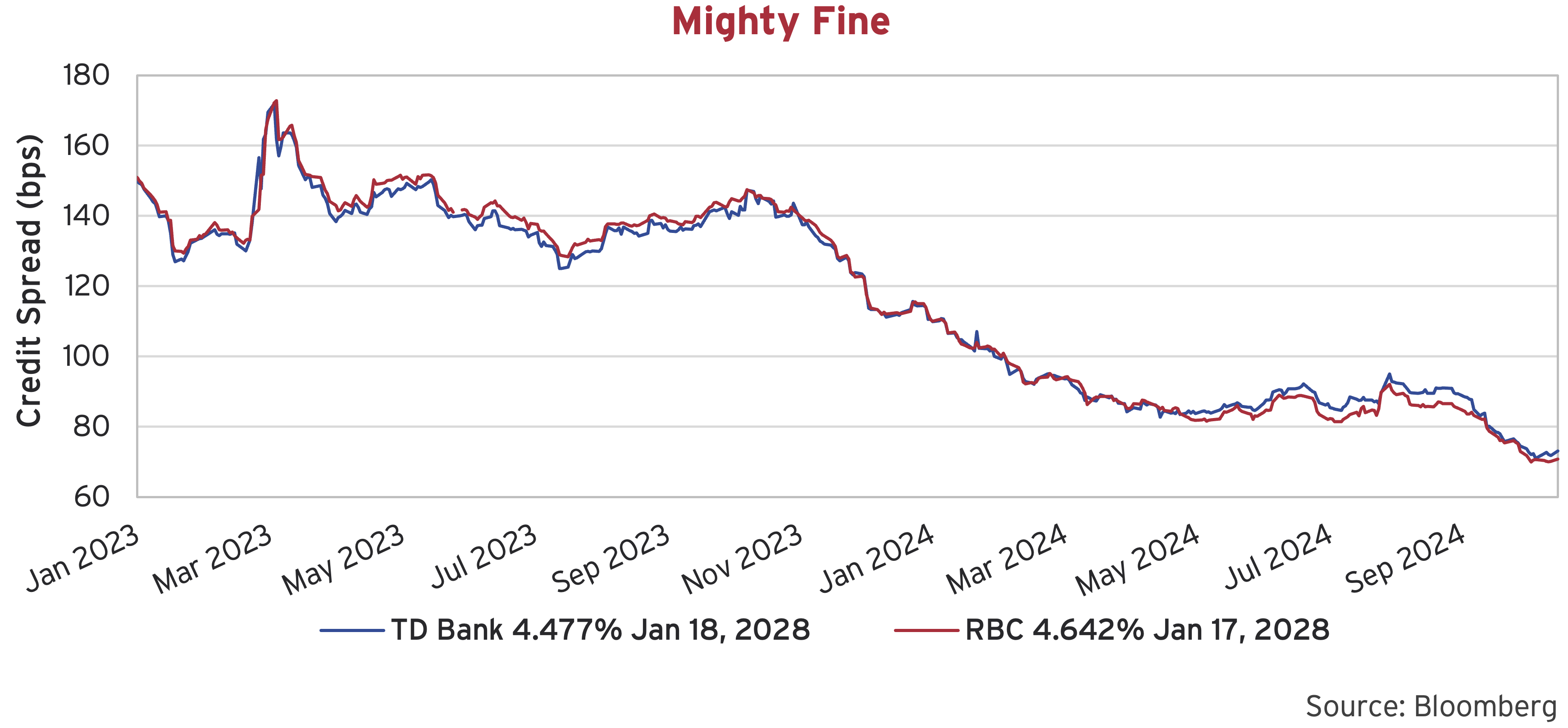

Mighty Fine

TD Bank’s money-laundering probe culminated with a guilty plea and fines surpassing US$3 billion. The issue first came to light in May 2023 when TD surprised the market by pulling out of their First Horizons acquisition due to “regulatory approvals”. There was initial speculation that TD opportunistically stepped away from the acquisition, given the U.S. was in the midst of a regional banking crisis. But three months later, the Bank confirmed a formal investigation was underway.

TD has spent the better part of the past year overhauling its systems and strengthening its internal compliance team. The guilty pleas are part of a coordinated resolution across multiple U.S. regulators and law enforcement agencies. TD’s CEO apologized for the Bank’s shortcomings and announced he will retire as CEO in 2025. The Bank’s share price has bounced up and down over the past year but is largely unchanged, down only 5% since the regulatory issues first came to light. Credit spreads, on the other hand, have shaken off the negative news and continue to march tighter alongside Canadian peers.

The Bottom Line

It was a subdued start to the summer within fixed income markets. Angst over unemployment data and underwhelming earnings sent yield spreads sharply higher headed into the August holiday weekend. No summer vacations needed to be canceled though, as markets quickly rebounded and with it, any buying opportunities. The Fed’s path to monetary easing was unimpeded and for now, the economy continues to prove resilient. Both risk assets and safe havens posted strong finishes for the third quarter. A decline in yields, tighter corporate credit spreads and robust fund flows positively impacted fixed income markets, while equity markets shrugged off mixed economic signals, ascending to record highs.

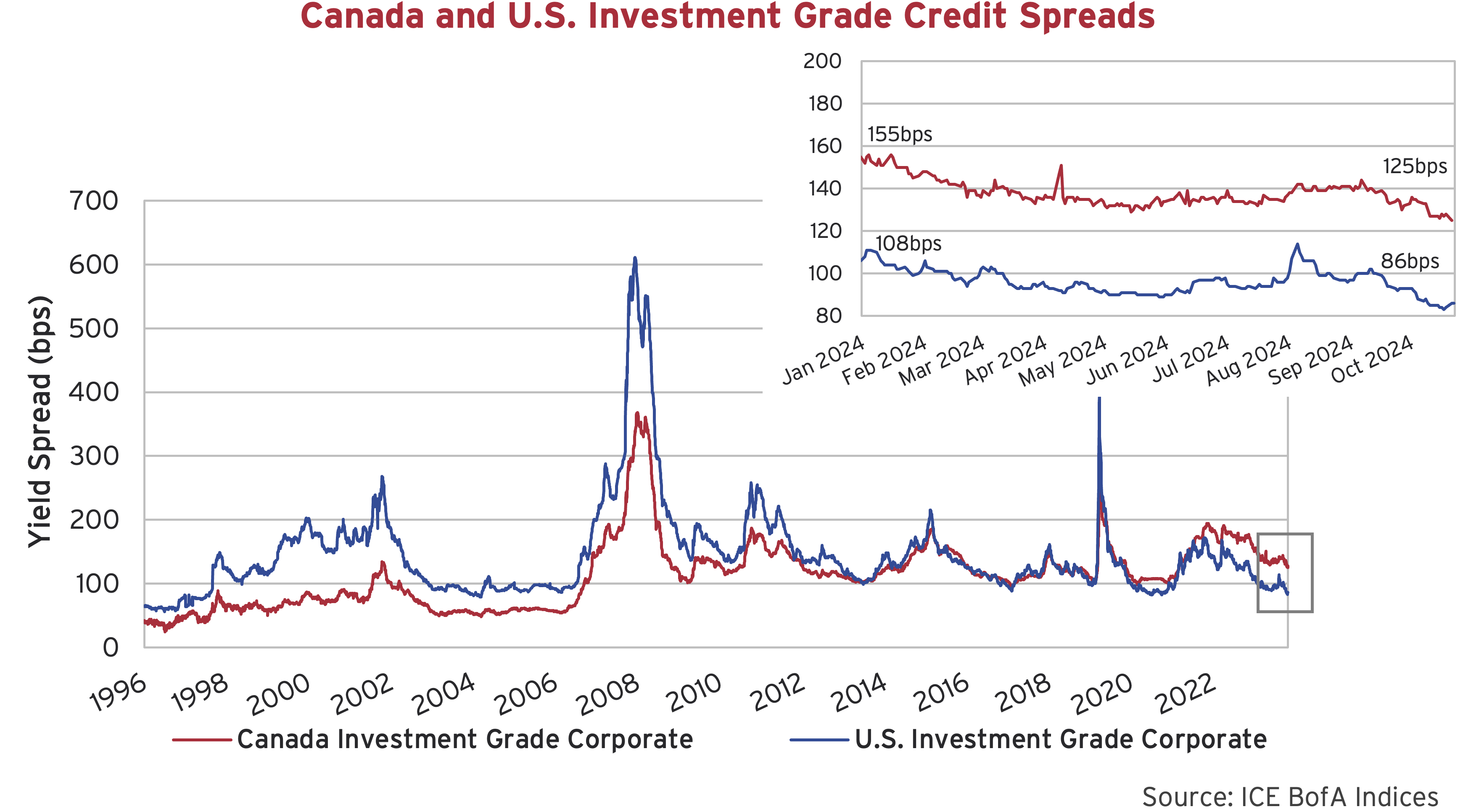

Corporate Action

Canadian investment grade credit spreads widened alongside broader market volatility in the month of August before rallying in September to end the quarter 4 bps tighter than where they started. The U.S. Investment Grade Index plotted a similar path, but as is normally the case, volatility was more pronounced. Investment grade spreads have now touched 83 bps in the U.S., the slimmest borrowing premium since Mats Sundin was captain of the Leafs back in 2005.

Through the first three quarters of the year, Canadian investment grade spreads have tightened 19 bps and the U.S. 13 bps. Canadian financial issues have been slowly closing the gap with the rest of the corporate market since significantly underperforming in 2022. Canadian BBB-rated issues have also performed relatively well this year, but in absolute terms are much wider than down south, particularly within longer term bonds. While the basis between the two has been grinding tighter, the Canadian market still has room to run to reach previous cycle tight levels. The U.S. can’t say the same, looking quite expensive with spreads much closer to all time tights.

In the U.S. High Yield market, demand for yield continues to be resilient as investors look to lock-in and benchmark focused managers are forced to accept a meagre risk premium to stay fully invested. Credit spreads ultimately finished the quarter 13 bps tighter, which contributes to a total of 46 bps tighter so far this year.

Summer Sales

Investment grade new issues continued to be well received by investors. Canadian new issue volumes remained very healthy in the third quarter and are tracking well above last year’s pace and not too far from record levels of 2021. Last quarter the market embraced the record issuance from Coastal GasLink that tallied $7.15 billion across 11 tranches. The most recent quarter saw banks and other financial issuers continue to be active, with EQB Inc. opportunistically placing their inaugural LRCN debt deal in the Canadian market, building an order book that was 4 times oversubscribed. Additional corporate issuance came from Telus, Enbridge and the inaugural transaction from South Bow.

TC Energy Corporation completed the spin-off of its liquids pipeline business into another company called South Bow Corporation. The South Bow assets include the Keystone pipeline that carries oil from the WCSB in Alberta to refineries in Illinois and Texas. The pipeline also connects to a distribution centre in Cushing, Oklahoma. South Bow came to the market with several new issues in the U.S. and Canada including senior debt issues tallying US$3.65 billion and C$1.45 billion. Strong demand for the bonds in Canada allowed the CAD issues to price nearly 10 bps through USD levels. There was also US$1.1 billion in hybrids issued into the U.S. market.

Check’s In The Mail

On September 4th, fixed income investors also lined up to purchase $1 billion of a new corporate bond deal from Aspen Investments LP. With due diligence complete, indications in, and the order book divvied up, investors sold existing holdings to fund the settlement of the new bond, scheduled for September 9th. Like any of the many other deals brought to the Canadian market, everything appeared to be proceeding as normal. What followed, was anything but:

“The collapse of the bond sale marks the first syndicated Canadian-dollar bond deal to be canceled, according to Bloomberg records.” Source: Historic Bond Deal Failure Was Result of Financial Model Error, Scotia Says. BNN Bloomberg. Xu, Chunzi. (2024, September 10).

Five weeks earlier, TC Energy announced the sale of a 5% equity stake in two Alberta-based pipeline systems to a consortium of Indigenous Communities (to be named Aspen Investments LP). TC Energy is no stranger to large transactions, buying and selling assets across North America is normal course business for the company. The transaction also benefited from significant support from the provincial government. Despite this, mysteriously, the transaction failed to close at the last minute. Why the deal failed remains unclear, with “transaction structuring issue” being the only explanation provided. Speculation is that the parties could not come to an agreement on the modelled cash flows, or that the model itself had an error in it – something that presumably would have been checked well in advance of closing. TC Energy agreed to make investors whole following the mishap.

Shifting Down Under

The Australian Prudential Regulation Authority (APRA) has proposed changes to its capital framework for banks. If adopted, the use of hybrid bonds such as Additional Tier One (AT1) securities will be phased out by 2032 and replaced with Tier 2 and Common Equity Tier 1 capital.

AT1 bonds were originally introduced in the aftermath of the global financial crisis as part of an investor ‘bail-in’ regime designed to reduce the likelihood of bailouts funded by the taxpayer in future crises. The 2023 regional banking crisis exposed the shortcomings of these securities, when a number of governments were forced to intervene in order to mitigate the risk of financial system instability. Swiss regulators wrote off CHF16 billion of Credit Suisse’s AT1 bonds (~10% of the global AT1 index at the time) as part of the UBS rescue. These events have informed APRA’s view that AT1 bonds fail to fulfill the function of stabilizing a bank in crisis due to their complexity, the potential for legal challenges, and the risk of contagion.

Australia’s AT1 market is unique among its global peers because of the high participation of retail investors that hold about half of the total amount on issue. This heightens some of the risks associated with AT1 in Australia. In our home market, Canada’s regulator, the Office of the Superintendent of Financial Institutions (OSFI), restricts retail eligibility through minimum denominations, and to date, has not expressed a need to review the efficacy of AT1 instruments. Nonetheless, we will watch the developments at APRA with interest and its impact on Australia’s A$39 billion AT1 market.

Warning Bell

During the quarter, Moody’s downgraded Bell Canada to Baa3 from Baa2, one notch above junk. Shortly following the downgrade, it was announced that Bell is selling its ownership stake in Maple Leaf Sports & Entertainment (MLSE) for $4.7 billion to competitor Rogers Communications. The two telecom companies shared their 37.5% each ownership for the past twelve years. Rogers will now own 75% of MLSE if the regulators and sports leagues sign off on the purchase. Rogers, who also owns the Toronto Blue Jays, is keen to win subscribers who watch live sports as the company is losing cable customers to streaming services. How the acquisition of trophy assets affects Rogers’ already high leverage levels remains to be seen.

For BCE, the deal makes sense to us. After its credit rating has now been downgraded by two different rating agencies, the equity sale allows the company to direct proceeds to reduce debt. Leverage has increased at BCE over the past several years as the company has spent heavily on installing fibre network in more neighborhoods and the mobile phone industry in Canada remains competitive. The company is working to right size its workforce, but has not yet addressed whether its dividend needs to be rightsized as well.

Not Just Another Notch

This past quarter Boeing was also put on notice, with S&P placing its credit rating on CreditWatch Negative. Boeing currently sits just one notch above junk from S&P, Moody’s and Fitch. Given that it is rated by all three agencies, it would need to be downgraded by 2 of the 3 before falling out of most investment grade indices. If this were to occur, with US$52 billion of index-eligible debt, Boeing would be the largest fallen angel on record.

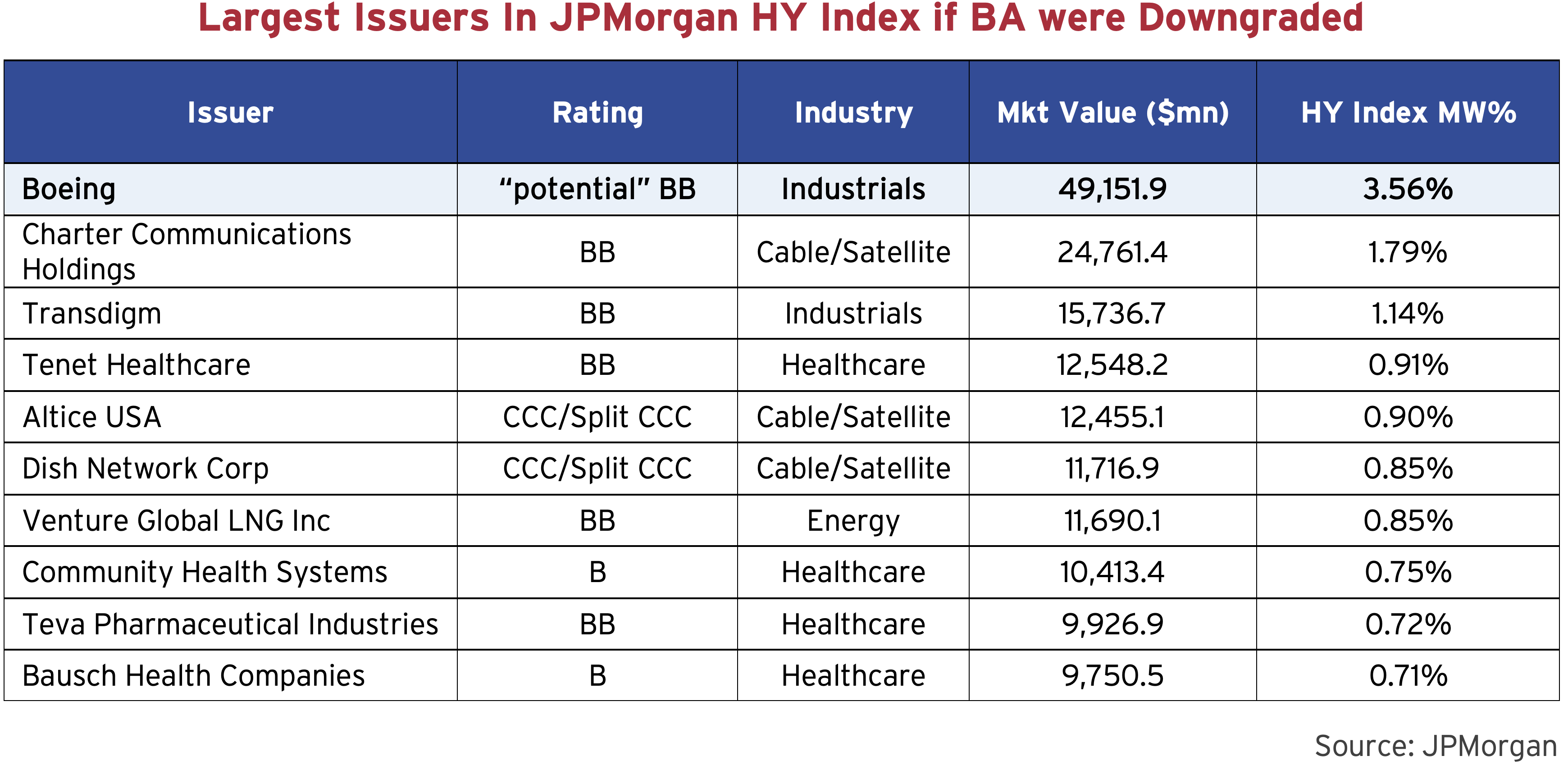

In addition to potentially being the largest fallen angel, Boeing would also become the largest issuer in the U.S. high yield bond market. In the chart below, JPMorgan has calculated the impact of Boeing being included in its high yield index. Moreover, Boeing has a large proportion of long tenor bonds outstanding, which is not normally found within the high yield market. The good news is that, at present, credit spreads at Boeing remain well behaved. Market liquidity is also strong, which could help to offset any forced selling in the event of downgrade.

Junk Status Update

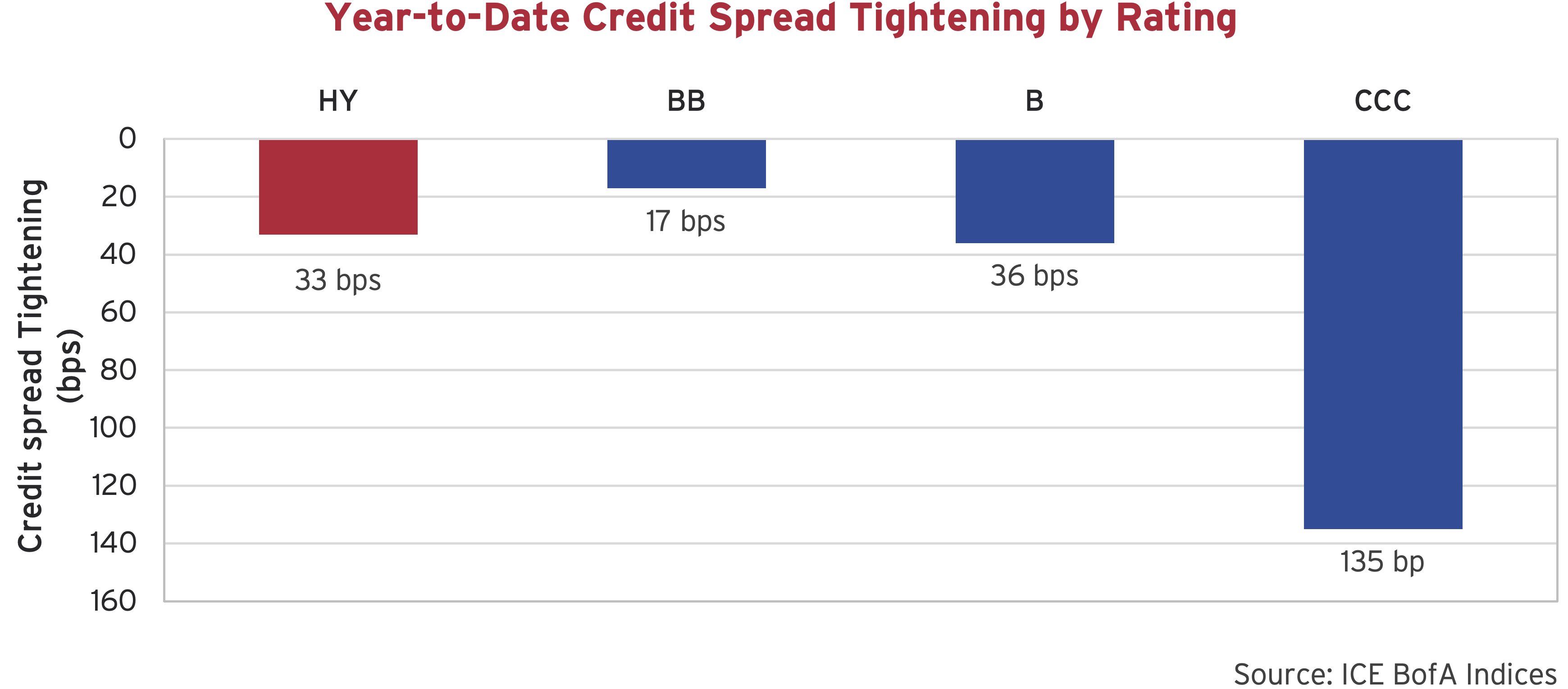

Through the first half of the year, we highlighted the outperformance of the single-B rated segment of the high yield market. At that time, single-B rated bonds sat at multi-year tights and accounted for the majority of spread tightening within the high yield index. Lower quality CCC rated bonds didn’t move much for most of the year, but that changed in this past quarter. Bonds rated CCC & lower were 152 bps tighter in the third quarter, relative to BB and B rated bonds, which were marginally wider. Year to date, the lowest quality bonds are now outperforming.

The tightening within lower quality CCC-rated bonds has been driven by outperformance in just a few issuers. Dish DBS Corporation bonds surged at the end of September, following rumours that parent company EchoStar was in talks to merge its satellite TV business with DirectTV. Once the deal was announced, EchoStar launched a series of exchange offers and consent solicitations with Dish DBS noteholders to permit the acquisition. Following the initial exchange offer, DirectTV will implement a mandatory exchange offer, swapping the newly exchanged notes into new DirectTV notes at a discount to par. After the announcement, S&P Global Ratings downgraded Dish DBS to CC, from CCC- to reflect the loss relative to par for the original bondholders.

Another larger mover in the quarter was CommScope Holding Company, whose bonds also rallied after the company entered into an agreement to sell its outdoor wireless networks and distributed antenna systems business for cash. Pitchbook has reported that the company has been engaging in negotiations with its creditors for a potential liability management transaction. The company may look to implement a dropdown transaction, where the company could raise new debt and launch an exchange offer to address debt coming due next year.

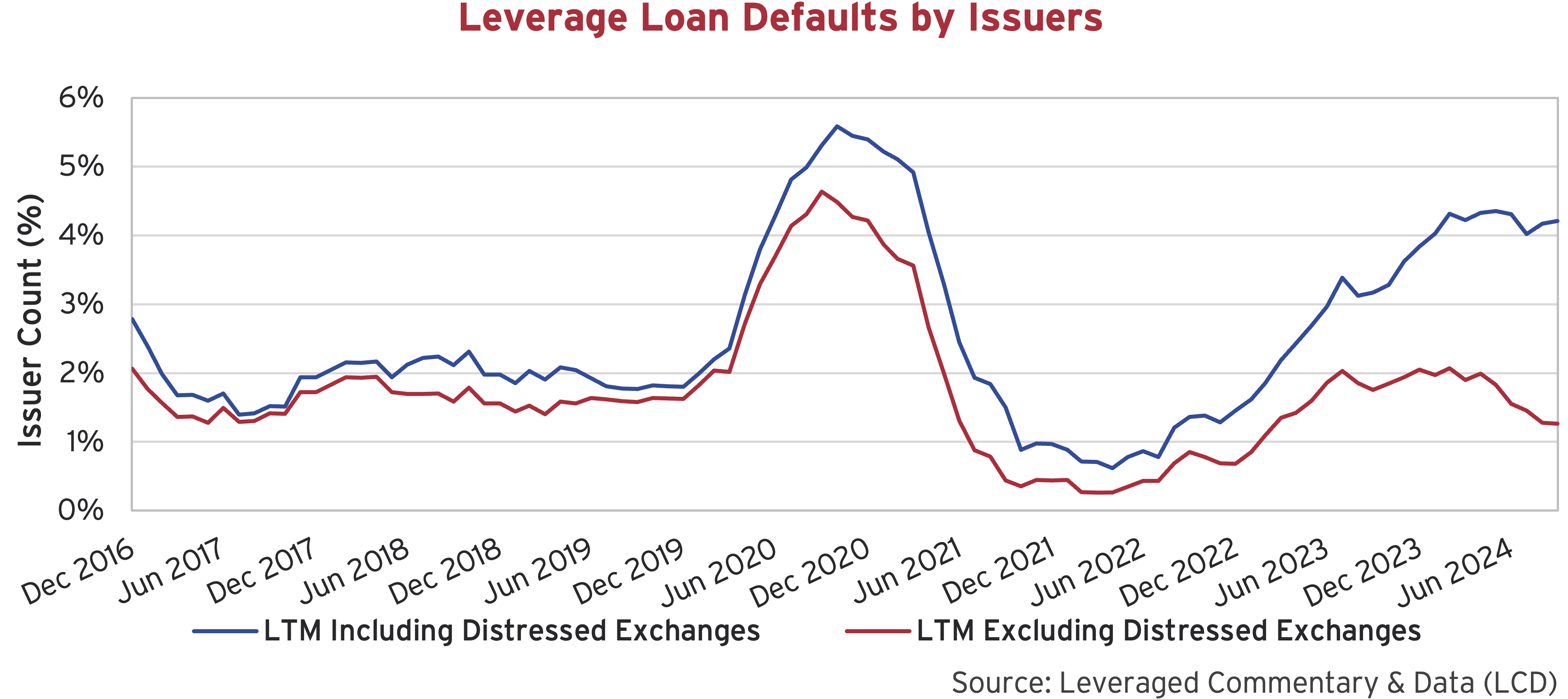

In our previous newsletters, we have talked about the increase of “Distressed Exchanges” or “Liability Management Transactions” in the market. These transactions typically involve moving assets and collateral to different subsidiaries or introducing new ranking levels within a company’s capital structure. The examples above highlight what is becoming increasingly common, albeit more pronounced within the loan market. We can see from the graph below that while defaults continue to taper off, distressed exchanges have become an increasingly common lever. According to JPMorgan, 32 companies have completed a distressed exchange this year totalling a record high US$7.8 billion in bonds and US$29.9 billion in loans.

Broken Record

We may sound like a broken record but as long-term investors our investment views don’t usually change from quarter to quarter. More importantly, our investment philosophy doesn’t change from cycle to cycle. We view high yield credit spreads as priced for perfection, and don’t feel as though we are adequately compensated for assuming this risk. If that means foregoing yield in the short-term and improving quality, so be it. We will be patient. Liquidity is our focus at this stage in the cycle, as too often we are reminded that investments are easy to buy, hard to sell.