Arrivederci Roma

“Spicy Italian” politics sure took a bite out of the financial markets last week. After the populists ended up ascendant in the recent Italian election, the proposed coalition government composed of the anti-establishment Five Star and right-wing League parties failed on the Launchpad. Doubts over their commitment to the EU resulted in an abrupt Presidential repudiation and a potential constitutional crisis. Italian bonds, the Euro and risk assets around the world plunged on the unlikely prospect of an Italy outside the EU. Bond yields dropped on the “risk-off” market sentiment in other countries, including the US.

Within the walls of the Vatican, the Holy Father’s singling out of credit derivatives as “a ticking time bomb” a few weeks ago proved prescient as the cost of insuring Italian institutions “exploded”. The good news was that the fractious Italian populists look like they are forming a government that might not actually be as diabolical to the European Union and the Euro as feared by the markets.

The Italian fiasco, at least temporarily, overshadowed the ongoing British Brexit folly. Uncertainty on critical issues of immigration, regulation and trade in a post Brexit world did not prevent millions of Britons from watching the latest Royal Wedding as Prince Harry tied the knot with Meghan Markle. Who needs the EU when you’ve got the monarchy?

We’re Here for a Good Time

Speaking of royalty, why is Canada the only place in the world to celebrate Queen Victoria’s birthday? Between their BBQ and beer, the good citizens of Canada seldom pause to reflect on why they celebrate the birthday of the late Queen even though she was deemed to be the “Mother of Confederation.” Canadian James Paxton no-hit the Jays to a win in Toronto which oddly was cause to celebrate but the Winnipeg Jets’ incredible playoff run came to an end 3 wins short of the Stanley Cup finals.

What’s an Ontario Voter to Do?

Ontario voters might need their beer. As the Globe and Mail just said, “What’s a voter to do?” The Ontario Progressive Conservatives led by the controversial Doug Ford, are doing their best to squander their chance at forming a government as the NDP surges. It doesn’t help that the normally fiscally prudent Conservatives put out a costing on their campaign promises that didn’t include many numbers!

Liberal Premier Kathleen Wynne announced she knows the jig is up and an election loss is imminent. This seems to be an attempt by the Liberals to salvage the anti-Ford vote. Since the NDP is currently tied with the Conservatives in the polls and NDP Leader Andrea Horwath seems reasonable compared to the Trumpian Doug Ford, the “Never-Ford” vote just might go NDP. No matter which way the election goes, Ontario’s finances seem destined to deteriorate. Whether Ford or Horwath forms the government, their spending promises will make a bad budget situation even worse.

Through the Looking Glass

Things recently have had a surreal feel to them. One has to really wonder what is causing this departure from reality. The environmentally sensitive Canadian government headed by Justin Trudeau just agreed to pay $4.5 billion for Kinder Morgan’s Trans Mountain Pipeline and Albertans cheered! This was a far cry from the jeers of 40 years ago when the hated Feds created national energy champion Petro-Canada. Conservative Albertans railed against “Communist” Pierre Elliott Trudeau, Justin’s father, and wanted to let the “Eastern Bast#@ds Freeze in the Dark”.

In the Looking Glass world of Trump Washington, there is no doubt about who is the Mad Hatter. The formerly free trading United States and Republicans are now tossing Trump Tariffs at close allies while making nice with NORTH KOREA!! This is all to make points with Trump’s CONSERVATIVE (??) base. Canada, the US and Mexico continue the NAFTA debate but the Trump administration is playing hardball. They just let the aluminum and steel tariff exemptions for Canada, Mexico and Europe expire. These astounded and close American allies are now planning to levy retaliatory tariffs of their own. We will soon find out if Trump’s Twitter assertion in March when he put on the tariffs that “trade wars are good, and easy to win” is true.

Since we are students of history we point out that everybody is usually enthusiastic at the start of a war. They very quickly lose their patriotic fervor when the casualties start to mount. A lot of Trump supporters are going to be very upset when prices go up and their jobs, businesses or farms suffer. The steel tariff is already hurting US manufacturers who use imported steel as their clients import cheaper finished products made with cheaper foreign steel.

The Canadian Bond World is Flat

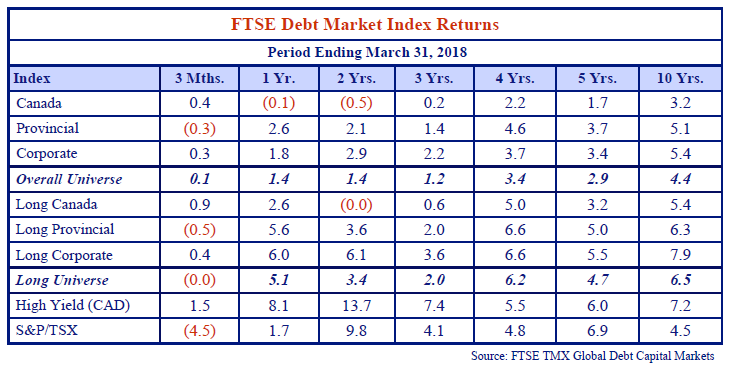

Canadian bond market returns were flat over the first quarter. The FTSE Universe Index returned 0.1% for the quarter and a meager 1.4% for the latest 12 months ended March 31st. The FTSE Corporate Index outperformed the Universe generating returns of 0.3% and 1.8% for the 3 and 12 months ended March 31st.

Up, Up and Away?

Interest rates and bond yields are still in a general uptrend. The US Fed again raised rates in March citing continued strength in the US labour market. This is the Fed’s sixth increase since it began raising rates in 2015 and it looks like more are in store with recent strong US economic statistics.

Things are so good that President Trump could not stop himself from tweeting out the good news on the May BLS Employment Report: “Looking forward to seeing the employment numbers at 8:30 this morning”. The Tweeter in Chief unfortunately broke years of protocol by commenting before the official release and the market immediately reacted. Bond yields and the US dollar rose on the now expected positive economic news. The report actually was very good with 223,000 new jobs created and the unemployment rate falling to 3.8% which equalled the booming 1990s and was only lower in 1969! We hate to be party poopers but 1969 was just before inflation took off in the 1970s. The US Fed kept monetary policy very loose in the face of high government spending and deficits. Sound familiar??

The Bank of Canada kicked off 2018 with a 25bp rate hike in January, the BOC’s 3rd such move in less than 7 months. Canadian long bond yields went the other way with a 4bp fall in the long Canada yield as trade worries sparked a bid for long term bonds from insurance companies and pension funds.

It’s An Easy Game

Friends and neighbours constantly remind us how much money they’ve made in the markets. Everyone, it seems, was an early investor in Bitcoin only to convert to a sage short seller at just the right time. Whether a midnight toker or not, all seem to have made a boatload on the marijuana mania in Pot stocks. And who didn’t own online shopper Ocada when it jumped nearly 50% after its tie up with Kroger! In an instant gratification world, fixed income seems outrageously pedestrian and old school.

Well, surprise your rich friends at the next block party when you tell them the FTSE TMX Bond Index (which is meant to represent the Canadian bond market) returned an average 4.4% per year over the last 10 years versus the S&P/TSX return of 4.5% per year over the same period. Had you invested in the FTSE TMX Corporate Bond Index your return would have been 5.4%, 90bps better than 4.5% return of the equity market. Not bad for a bunch of coupon clippers.

Now we must admit that this attractive historical return will be unobtainable starting from the current low level of bond yields. Starting with Canadian bond yields at under 3% and interest rates rising, it looks to us like even a 3% return will be difficult to achieve going forward. Despite this, it shouldn’t shock you when we suggest there is room for bonds in everyone’s portfolio. We would argue a bond component is as critical to a sound investment plan as rain is to farming. You don’t want too much of it, but too little can ruin everything.

And the Rain Came Down

To continue, we are often asked “why should I invest in fixed income at all?” One problem is that people confuse “Bonds” and “Fixed Income”. A bond is debt, a tradable promise to pay interest along the way and principal at maturity. Fixed income refers to the fixed in dollars nature of the coupon, the promised interest payment on most marketable bonds. Bonds can also have floating rate coupons which move up and down with the movements in short term interest rates.

Bonds provide diversification. Stocks have considerable price risk. Most investors need some income investments, or they could be forced into liquidating part of their portfolio when financial markets are rocky and prices are down. Marketable portfolios can generate income from bonds, dividend paying stocks and short-term money market instruments. Within bonds, investors can turn to corporate bonds to increase their income beyond what is paid by safer government bonds.

The choice between fixed and floating rate bonds is important. As interest rates and yields increase, floating rate bonds experience increasing interest income which moves up with market rates. Fixed rate bonds actually fall in value as new bonds become available at higher interest rates. Fixed rate bonds go up in value as interest rates fall since new bonds pay lower interest rates making existing bonds more valuable. This means there is a place for both fixed and floating rate bonds in the income portion of a portfolio.

To review the role of bonds in portfolio management:

- A generator of income. We suspect some of our readers may remember the 1980’s when GIC’s paid close to 20% and clipping coupons required large scissors and really meant something. Today’s yields in the low single digits provide investors less income (inflation is lower too) but it is still cash flow and cash flow helps pay the bills.

- A portfolio diversifier. Prudence dictates even the most aggressive investor refrain from putting all their eggs in a single basket. Fixed income acts as a diversifier and risk mitigator versus other asset classes. These include equities and real estate which tend to dominate portfolios for retail investors.

- A preserver of capital. No matter what you are saving for, a near term purchase of a car, sending your granddaughter to university 15 years from now or to pay employees’ pensions 30 years from now, you want to ensure the money you set aside to achieve those goals does not shrink and grows over time. Fixed income can and should act as a preserver of capital.

People Don’t Expect to Lose Money in Fixed Income

Another question we are asked is how we are going to make money in the future and, more importantly, how much? Implied in this question is the assumption we won’t ever lose money. The markets are 10 years into a period of extremely cheap money. Cheap money fuels greed and complacency which leads to asset bubbles.

In periods of low yields and tight credit spreads investors are tempted to (and often do) reach for yield by buying longer term securities with modestly higher yields (accepting more interest rate risk) or moving into more speculative securities (accepting more credit risk). We believe implementing either of these strategies in today’s market is a recipe for disaster. Unfortunately, many investors are doing both. So, while people do not expect to lose money in fixed income many have now set themselves up to do just that.

It is as important to understand how not to lose money as it is important to make money. Reaching for yield out the yield curve or down in credit quality is very dangerous right now. Don’t believe those who tell you it’s a new era or that we’ve reached a “new normal”.

One Direction

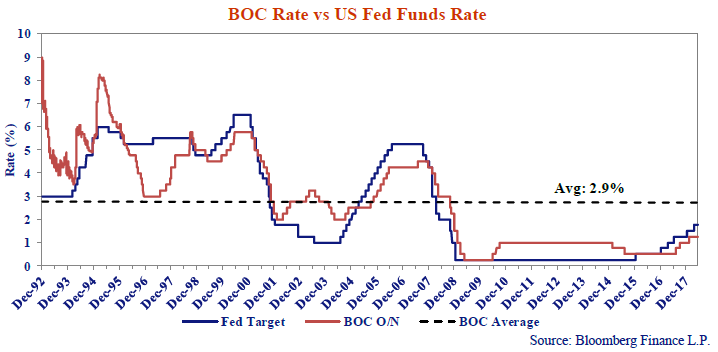

What can Canadians expect for interest rates going forward? Our answer is the name of the recently disbanded boy band. We expect interest rates to move in “One Direction” – higher. On the bond front we think yields will follow short-term interest rates higher in Canada, the US and even eventually Europe. This trend is already well underway. The chart below shows changes in administered rates in Canada and the US. Administered rates are controlled by the Bank of Canada and Federal Reserve.

In response to the Credit Crisis, central banks dropped administered rates to extraordinarily low levels. This response was intended to, first, stabilize the financial system and, second, to stimulate economic activity. In the US and Europe, central banks followed this up with quantitative easing, or QE, involving the purchase of trillions of dollars of bonds to maintain low rates and drive them lower.

Because of the actions of central banks, rates have stayed low for nearly a decade. Only recently, in response to consistent economic growth in the United States and Canada, have central banks very hesitantly started to move administered rates higher.

Too Low for Zero

We know the current preoccupation of central banks is to move interest rates higher to more “normalized levels”. Yet the Bank of Canada and Federal Reserve only directly control short-term interest rates through monetary policy. Global central banks resorted to buying bonds through their “Quantitative Easing” programs as a response to the Credit Crisis and the Euro Debt Crisis but are currently cutting back on these programs.

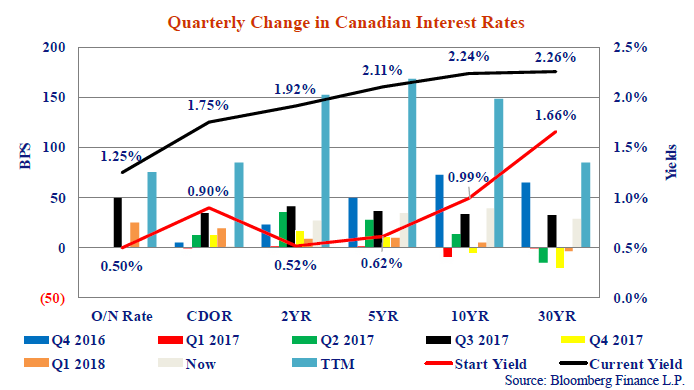

The chart above shows changes in yields by quarter going back to the end of September 2016 with the then and current yield curves overlaid. Despite being very low, interest rates in Canada are well off the bottoms. In 2016, yields on 5-year Government of Canada bonds bottomed at 0.50% and 30 years 1.55% versus 2.1% and 2.3% today.

We wouldn’t suggest current yields are overly generous but they are much higher than they were just a few short years ago. With inflation at 2% we are now at least approaching positive real yields across most of the yield curve. That said the risk to further yield increases is very real. What do rising administered rates and an end of bond buying by central banks now imply for longer term rates?

Moving On Up…To The Top

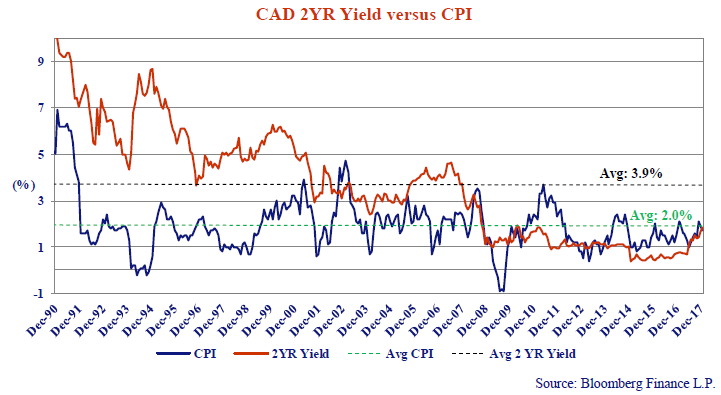

Rates are on a gradual path to normalization. Over the cycle, we expect yields to approximate inflation, currently hovering around the mid-point of the Bank of Canada’s 1 – 3% band, plus one or two percent. This relationship suggests a 2-year Government of Canada bond yield of 3 – 4% and with a positively sloped yield curve, implies 30-year yields of 4 – 5%.

Per the chart above, since the Bank of Canada began targeting inflation in the early 1990’s, 2 year yields average 3.9% with inflation at 2.0%. With 2 and 30-year yields at 1.9% and 2.3% today markets have a long way to go to get anywhere near normal. We may not get to a 4 – 5% long bond this year but we think eventually that is where it will wind up.

And Another Thing!

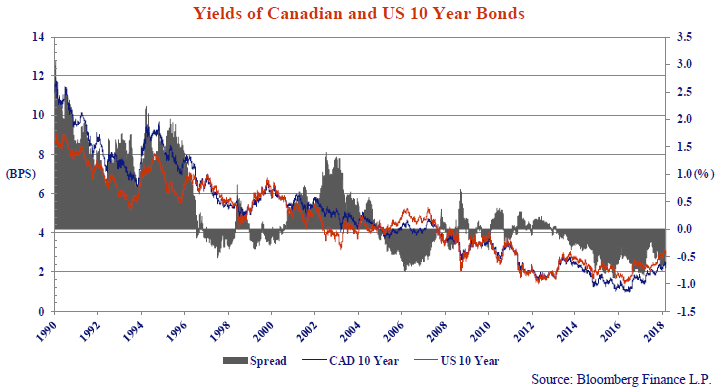

Historically the Canadian government paid more to borrow money than the US. Across the yield curve, Canadian rates are currently less than US rates. The concept of normalization applies to both an increase in the general level of interest rates as well as elimination of the premium of Canadian bonds versus US treasuries.

Since 1990, on average, 10-year Government of Canada rates are 30bps higher than 10-year US treasuries. They have averaged 22bps lower since the Credit Crisis whereas prior they averaged 56 bps wider. Today, 10 year Canada’s are 60bps lower in yield than the corresponding US treasury.

Why? Through the Credit Crisis, the Canadian financial system (and Canada generally) is widely perceived to have held up better than the US. There was less risk and less risk taking in Canada than the US and Canada was rewarded for that. The perception Canada was a safer place to invest manifested itself in lower yields for Canadian government bonds.

Sovereign yields should ultimately reflect the credit quality of the country relative to others. While we are patriotic, we believe the US economy is in better shape than Canada’s and is a better-quality credit risk. Canadian yields should revert to “normal” levels, that is, higher than the US.

So, we see three drivers pushing Canadian interest rates higher. First, Bank of Canada administered rate increases, which are expected to track but not mimic expected Federal Reserve increases. Second, longer term rate normalization to +1 to +2% above inflation. Third, credit normalization to reflect stronger US economic fundamentals versus Canada.

The Real Problem

There are potential headwinds to rate increases. Canadians are heavily indebted and as the Bank of Canada increases short term interest rates, interest payments on lines of credit and floating rate mortgages rise. Fixed rate mortgage rates rise as Government of Canada 5-year yields rise. These interest rate increases will take a larger bite out of the take home pay of Canadians.

At Canso, we called the beginning of the end in Canadian residential real estate in mid-2013, so, suffice to say, we’ve been really early. Nearly five years on, storm clouds are gathering over the residential real estate market with both Toronto and Vancouver well into an unravelling. The recent numbers in Vancouver and Toronto show a significant fall in both the number of transactions and transaction prices.

The market has been primed to lofty valuations and excess by very cheap money which is going away as rates rise. This combines with a tightening of regulation with the introduction of B20 mortgage rules. Mortgage underwriting fraud through income falsification and money laundering through residential real estate are both now belatedly getting the attention of Canada’s politicians and bureaucrats. There’s nothing like getting asked by your boss about a newspaper mortgage fraud story to increase mortgage underwriting standards. The scope of mortgage fraud is breathtaking and is only now starting to be understood.

Depending on the breadth and the depth of the unraveling and its impact on economic activity, interest rate increases by the Bank may slow but we still believe the path is to higher rates.

Defence is the Best Defence

So where do we stand?

- Everyone should be at least partially invested in fixed income. √ Check.

- Interest rates are expected to go higher. √ Check.

- Higher interest rates are bad for fixed income. √ Check.

Higher interest rates negatively impact fixed rate bonds. The longer the term of the fixed rate bond the higher the duration and the greater the negative impact. For example, 30-year Government of Canada bonds yield 2.3% today. Should long rates move to 3.3%, it is logical the bond with a fixed coupon of 2.3% would fall in value, as a matter of fact, it would fall ~20% in value. A 2-year fixed rate bond would fall just less than 2% in price.

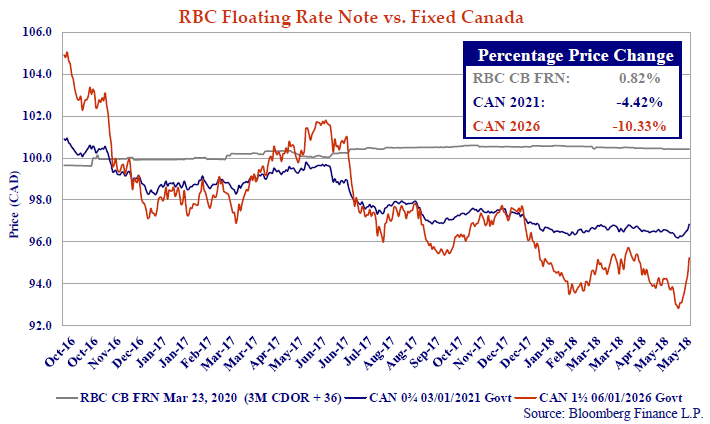

Things are not nearly as desperate as this suggests. Not all bonds are created equal and not all bonds react the same as rates move higher. In recent years, Canso’s bottom up relative value approach resulted in large purchases of floating rate notes. In a rising rate environment, floating rate notes hold their value as coupons reset every 3 months.

The chart above shows the price performance of a Royal Bank of Canada Floating Rate bond versus 5 and 10-year Government of Canada bonds. In a period where 5-year rates moved up ~170 bps the RBC Floating Rate Note, which resets every 3 months, increased in value while fixed rate Canada’s fell significantly.

Youse Payse Your Money and Youse Takes Your Chances

As they say in the carnival midway, “Youse Payse Your Money and Youse Takes Your Chances”. We like to know what our chances are. Lending money is a risky business but Canso is a specialized lender focusing on the Corporate Credit markets. As a lender to companies we must determine:

- Is the company going to pay us back?

- Are we compensated for the risk the company doesn’t pay us back?

- What happens if the company doesn’t pay us back?

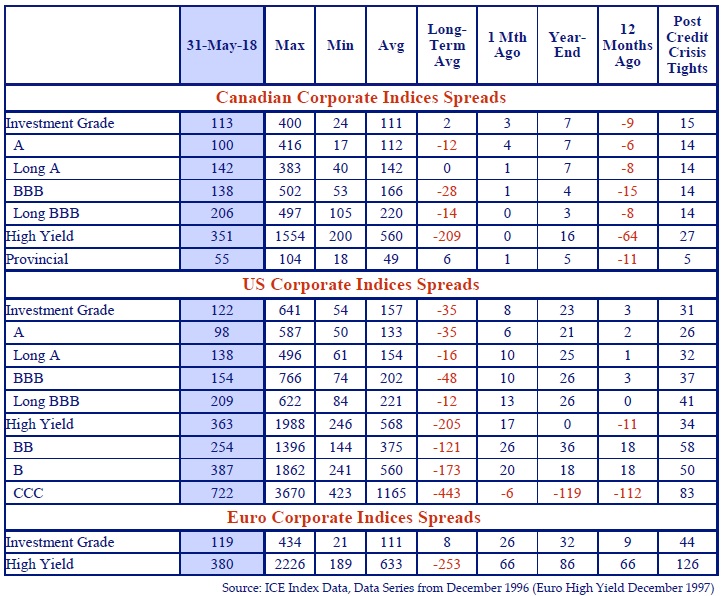

Compensation for assuming corporate credit risk is the incremental charge for lending to a non-government entity – or credit spread. The table below shows current credit spreads in Canada, US and European credit markets across select rating categories and terms. The comparative data cover monthly periods dating to December 1996.

On average in Canada since 1997, the incremental credit charge for an investment grade corporate is 111bps above Government of Canada bonds. At May 31, Canadian investment grade spreads were +113bps, just above long-term averages. Within investment grade, BBB rated bonds were 28bps tighter than historic. In US investment grade, spreads are 35bps tighter than average with BBB’s 48 tighter. All indices are slightly off the post Credit Crisis tights.

Party Crowd

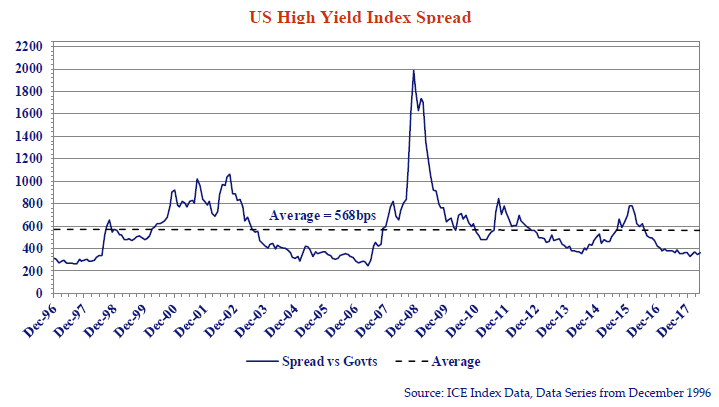

At May 31, the ICE Index US High yield spread measured +363bps or 205bps tighter than average of 568bps. Non-investment grade borrowers are borrowing at very attractive rates.

Per the chart above, in February 2016 US High Yield spreads of +775bps were over 4% wider than today. As a lender this translates to significantly lower risk compensation for advancing money to lower rated corporates.

Different or Really, Really Worse?

As credit spreads narrow, it benefits borrowers as they pay less to their lenders for the same risk. In recent years, as spreads tightened the contractual terms underpinning the lending relationship moved decidedly in the borrowers’ favour. So, it has been a great market to be a borrower – cheap money with fewer restrictions. Conversely, it’s less and less attractive to be a lender.

It is a founding principle of Canso that at market tops very shrewd underwriters create absolute garbage to sell to naïve buyers. We have seen this in every credit cycle and a key part of our success is to resist the lemming urge to throw these investments into your portfolios. This time is no different and looks to us to be actually worse in the lower quality credit markets. Yes, you might accuse us of being crotchety old lenders who are always out of investment fashion but we have evidence to back up our seemingly outlandish claims.

The contract governing a loan agreement includes “covenants” that protect the lenders. In today’s market, in the rush to get invested, these protections are being gutted with fewer and fewer covenants resulting in “Covenant Lite” bank loans, which we think are a credit abomination. These Covenant Lite loans are being stuffed into breathless buyers who have to invest their cash, no matter how stupidly. JP Morgan’s Leveraged Loan Research team noted in 2008 Covenant Lite loans comprised 3.5% of total loan issuance. In 2017, Covenant Lite loans comprised 78.6% of all issuance according to JP Morgan. Is this time different or really, really worse??

Companies get into trouble due to aggressive growth through acquisition or expansion strategies, excessive leverage, high cost structures or less frequently, but more spectacularly, fraud. The best way to reign in reckless behavior is to contractually limit management’s ability to undertake aggressive activities. Lenders who give away these protections do so at their own peril. Eventually as the cycle unwinds, and as the high yield spread chart above shows, the cycle always unwinds, credit spreads rise, defaults increase and recoveries fall.

Investors who have piled into retail oriented products – high yield bond funds, ETF’s backed by high yield bonds or leveraged loans – will ultimately lose. Structures employing leverage will suffer the largest loss of value. These products must be invested in high yield assets. Recall in 2008 the high yield market fell 26%.

Someday You’ll Understand

The fixed income markets seem more challenging than usual these days. Canso was founded in 1997 when investment grade credit spreads were 25bps over Canada’s versus the 110bps they are today. This was arguably the worst possible time to start a credit focused fixed income shop. Over twenty years on, we’ve outperformed through all types of markets proving there are opportunities in every market if you know where to look and what you are looking for.

As an active investment manager, Canso’s job is to generate positive returns consistently over long periods. Having said that, we accept that we may not outperform in every period, in every quarter or even every year. Sometimes the market dynamics suggest the best question to ask (which no one ever asks) is “how do I not lose money?” and not “how do I make money”.

The credit risks in the bond markets are real and the potential losses significant. These risks can be mitigated and losses avoided but one needs to be proactive to protect capital and then to take advantage of market dislocations to grow capital when appropriately compensated. Market calamities can be turned into opportunity. When people are panicking and selling, you want to be buying.

Maybe I’m Amazed

There are any number of analysts, journalists and investment managers who will tell you things are different this time and we’ve entered a “new normal” characterized by lower than historic yields and credit spreads. At Canso we don’t buy that and we don’t think you should either.

We believe the financial markets are inefficient. We generate long-term out-performance by being positioned to take advantage of opportunities we know will present themselves either from a general market selloff in rates or credit or both and select one-off special situations.

Opportunistically taking advantage in market dislocations just as we did in the Credit Crisis of 2008 and Euro Debt crisis in 2011 allows Canso to generate performance over the long term. We have two dozen investment professionals analyzing individual companies and when opportunities present we will take advantage.

Successful investing generates returns over long periods through the extremes of economic and financial cycles. Our singular mission is to deliver returns to those who have entrusted us with funds to manage. All of our employees invest in Canso funds ensuring the perfect alignment of Canso with its clients.