When the monetary authorities are forced to raise interest rates, they will likely do so hesitatingly and apologetically. They will then be forced to play catch up to be taken seriously by the markets. Rising rates will again not be kind to the credit markets. But what of the chastened and reformed bankers and investors, you might ask. Won’t they enforce greater credit market discipline after their brutal lessons from the credit crunch? If the current mania for junk bonds is any guide, the answer is a resounding NO!

It is premature, however, to exit risky assets to lock in the paltry interest rates on government bonds. Whether one argues that the 30 year bull bond market is over or that increasing government deficits will raise real interest rates, long duration governments are clearly not a place of refuge from market turmoil. The long U.S. Treasury yield is up to 4.5% from its low of 2.5% in the darkest hours of the credit crisis. This is a capital loss of more than 20%.

Performance Envy and the “Heinz Rally”

Theoretically and dogmatically, government bonds are suffering from the twin terrors of rising government deficits from loose fiscal policy and potentially rising inflation from loose monetary policy. Practically, government bonds have been clocked by the reversal of the “fear trade” and performance envy. Consensus investors who believed the terrifying financial press during the credit crisis and bought government bonds for safety have been since flocking to the risk and higher yields of corporate bonds. They are doing this because it is the consensus thing to do. They are also chasing the performance they probably missed during the huge credit rally of 2009.

Our clients and readers know that we bought cheap corporate bonds during the credit crisis and have been fully invested ever since. The consensus bond managers who sold corporate bonds and fled to the safety of governments during the credit crisis had a very hard time “getting invested” as spreads collapsed in the mother of all credit rallies. We call the current strong bid a “Heinz Rally” as it is smothered in “Catch Up” behaviour.

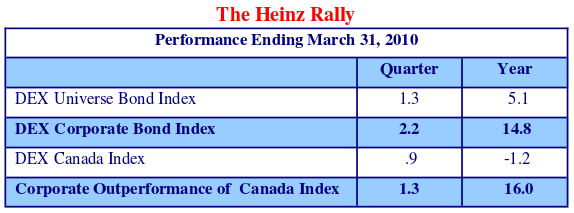

The reason for this pro-cyclical corporate bond accumulation can be seen in the table above. In the quarter ending March 31, 2010, corporate bonds outperformed Canada bonds by 1.3%. Over one year, corporate bonds outperformed Canada bonds by 16%. Since corporate bonds comprise 27% of the DEX Universe Index, the performance from this sector (27% x 16% = 4.3%) made up almost the whole return of the Universe.

A bond manager who was underweight corporate bonds by 10% versus the benchmark DEX Universe would have underperformed by 1.6%. A 20% underweight would have been the performance kiss of death at 3.2%. Given that bond managers typically don’t add much value above their benchmarks, a corporate underweight would not be popular with clients, consultants and even the fellow partners who argued for the “prudent” credit underweight during the credit crisis. Hence the mad scramble for credit product.

“Made (Poorly) in Canada”

We don’t really mind pro-cyclical and consensus investors bidding up the prices of our bonds, in fact we encourage it. On the other hand, as credit professionals, watching other bond managers snap up weak deals at very expensive prices is a tad dispiriting. The bid for corporate bonds is now so strong that investment dealers are back to their pre credit crisis trick of doling out corporate bonds like water in the Sahara. The oversubscription of new corporate issues runs at 5-10 times and fills of popular issues are 10-20%.

We are particularly unenthused over the “Made in Canada” new issue market for Canadian high yield bonds. The underwriters who created the income trust fee bonanza are now looking for a replacement underwriting fees to top up their bonus packages. They have hit on developing a Canadian high yield bond market. Their thesis is that since all the income trusts need to convert to corporations, due to the change in their federal tax treatment, they will need to lever up with debt to provide higher earnings and dividends. The corollary to this thesis is that the “High Income Funds” created to hold the flotsam and jetsam of Canadian income trusts will now need to replace these investments as well.

High on High Yield?

Unfortunately, the underwriters are committed to maintaining the proud Canadian tradition of issuing bonds with the worst structure and covenants in the world. Canadian investment grade bond covenants typically allow complete subordination of the bonds to the bank debt which is not the case in the U.S. or any other sane market. The recent crop of Canadian high yield issues has distinguished itself by removing the typical protections of U.S. deals. Indeed, on some simultaneous Canadian and U.S. dollar issues, the underwriters have chosen to have reasonable covenants for the U.S. issue and to use the zero protection Canadian style for the Canadian dollar issue. Obviously, we have not invested in any of these credit abominations.

Why, pray tell, do Canadian high yield investors not demand the same protections or even better than their U.S. cousins? Well, one of the reasons is that with all the money building up dedicated high yield funds, the portfolio managers must hold their noses and buy, even those that know better. The other reason is the emergence of a buyer who doesn’t know any better, the “equity buyer”.

Equity Buyers

In days of yore in the Canadian credit markets, a mere couple of years ago, a Canadian high yield bond was usually a fallen angel that had formerly been investment grade. A new issue high yield bond tended to be a closely negotiated transaction with security and proper covenants like the Viterra deals. There were 5-10 buyers, normally sophisticated investment counsels and institutions with their own credit capability.

In the currently sizzling “Made in Canada” high yield market, there have been 50-60 buyers of new issues. Most of these are termed “equity buyers” by their friendly bond salespeople and underwriters. To those of you who wonder why an equity buyer would be buying debt issues, this is again a uniquely Canadian twist to credit reality. The equity buyer is none other than the quintessential Canadian buyer of crapola masquerading as a yield product, the income trust manager.

Normally, yield products are the specialty of bond managers. During the Canadian income trust mania, many equity managers were given the duty of analyzing and buying the promises to pay 10% based on very mediocre cash flows and businesses. Perhaps it was thought by the sponsors of such funds that the upside of income trusts dominated their downside, so equity managers were given this new role.

For those of you unfamiliar with Canadian income trusts, this was a Ponzi scheme based on promising 10% yields on cyclical small, mature and otherwise undistinguished businesses to cash starved investors. All the upside was to the vendors, promoters and underwriters of these mediocre businesses. Their game was to promise 10% on issue no matter what the underlying reality of the businesses and distribute it pre-tax to investors. Canada became the global destination for selling businesses at the highest possible valuation. The result was “income trustification” of pet food manufacturers, tomato green houses, ice cube producers, knitting wool mills, coin operated laundries, coal terminals and many other small and/or cyclical businesses that otherwise could not have accessed the public markets.

The result was predictable. Many of the IPOs at $10 per unit ended up languishing or being privatized at cents on the dollar. When very large firms like Bell and Telus were forced to consider this structure to “maximize shareholder value” the federal government closed the tax loophole and killed the market.

As the market developed from the mid 1990s to the “Halloween Massacre” in 2006 when the tax loophole was closed, funds of income trusts were created to manage this new “asset class”. Now, the sponsors and managers of these funds are looking to morph their cash cows into new opportunities. The “Made in Canada” high yield market gave them a new raison d’etre and unleashed them on the unsuspecting bond market.

How To Implode a Bond Portfolio

This has not been a good thing for the high yield market in Canada. In our experience, a good way to implode a bond portfolio is to put an equity manager in charge of it. Equity managers are trained to see upside, not downside like a credit manager. In bonds, there is only downside to the promised return of a new issue. If a bond is bought at an original par value of $100 and the business does well, the credit spread might narrow, providing some limited upside. At maturity, however, the issuer is only obligated to repay the par value of $100. The maximum return on the position is therefore limited to the initial yield to maturity.

The downside to these issues dominates. For the equity buyers, ignorance is bliss. The investment dealers selling these defective wares make it very obvious in the prospectus that the recovery value will be zilch. The sales pitch to the equity buyers is that the high coupon is certain, unlike the income trust distributions they are used to. What the equity buyers don’t know will almost certainly hurt them. As lenders say, security doesn’t matter until it’s the only thing that matters.

They Know Not What They Do

The large senior debt claim with priority means that these issues could easily go to zero in a future bankruptcy. This would wipe out not only that position but the spread of many additional bonds in their portfolios. We have to forgive these credit neophytes for, in biblical terms, “they know not what they do”. An equity manager can have one stock increase 5 or 10 times in value which offsets the losses on other holdings. A credit loss in a bond portfolio will wipe out the excess yield of many other holdings. The current crop of “Made in Canada” high yield issues will have a very high default rate based on historical data. From the S&P surveys, a “B” rated bond has a 21% chance of default (globally) over the next five years. The historical defaults of a “CCC” rated bond is even higher at 45%. These are longer term “smoothed” statistics. As our clients and readers know, there is a credit cycle and defaults are bunched. The weak deals of speculative markets tend to become the defaults of credit contractions.

The coupons on the recent bonanza of Canadian high yield deals are 7-9% with a term of 7 years. This puts the spread over 7 year Canadas (3.5%) about 4-5%. If a couple of 3% positions in these bonds default, it would use up the entire excess spread of a portfolio. At Canso, we developed and have used our proprietary Maximum Loss to assess capital risk since 1998 for this very reason. Traditional credit ratings do not captured capital risk very well. The credit rating agencies have recently begun to publish “Recovery Ratings” to allow investors to judge the potential losses through default. It is instructive that several of the recent Canadian high yield deals are Recovery Rated 4 or 5 which indicates a loss of 50-80% of original par. We actually think the experienced losses would be worse and the bond holders would be wiped out in most of these deals.

Just Say No!

We have thoroughly analyzed and then passed on all of these deals, preferring to wait to buy them at distressed levels in the future. We have made our concerns known to the underwriters and the issuers to no avail. We are told that several of our credit peers, who know better, have been forced to buy for lack of other more sensible product. This is why we have never accepted a mandate that has a high yield benchmark. We refuse to set ourselves up for failure, trying to equal a benchmark that is inherently defective. We only buy riskier credits when we are well compensated for doing so.

The amazing thing to us is the cheek of the issuers and underwriters. Having issued in the U.S. market, the issuers know that the weak covenants and prior charge debt allowed are ridiculous. The underwriters know as well, but they are acting for the issuers. We asked the issuers to tighten up the covenants, particularly limiting the prior charge bank debt. Knowing the huge demand from the equity buyers, they politely decline to make a change and strike Canso off their list. At one meeting, when we asked to have the allowed prior charge reduced, the underwriters nearly burst out laughing!

It is sad that, for the fourth or fifth time by our count, the investment dealers of Canada are trying to develop a thriving high yield market in all the wrong ways. When the market turns south, the 50-60 equity buyers will turn into 50-60 panicked sellers and there will be no bids from their friendly Canadian dealers. A “Made in Canada” panic will develop and the overwhelming selling will crater the Canadian high yield market until the next cycle of greed. That’s when we will be buying.

Outlook

It is hard to predict when monetary policy will be tightened and even harder to predict when it will actually start to affect the financial markets. What we do know is the more money, the better it is for financial asset prices. The liquidity provided in the aftermath to the credit crisis was unprecedented, as has been the rally of the credit markets in response to it. We are still early in the recovery and it is unlikely that the Fed and other monetary authorities will tighten policy aggressively for at least a year or two.

We are typically early. In the summer of 2004 we believed that there would be another two years of decent markets before disaster struck. It turned out that the credit crisis began in mid 2007. By this time, our value discipline had taken us out of many of the cheap positions we had accumulated in 2002-2004 and our portfolios were quite conservative. One client asked us in 2007 how could we outperform with a more conservative and lower yield portfolio than the DEX Corporate Index. Our answer was that we would not expose the portfolio to excessive risk for very little compensation.

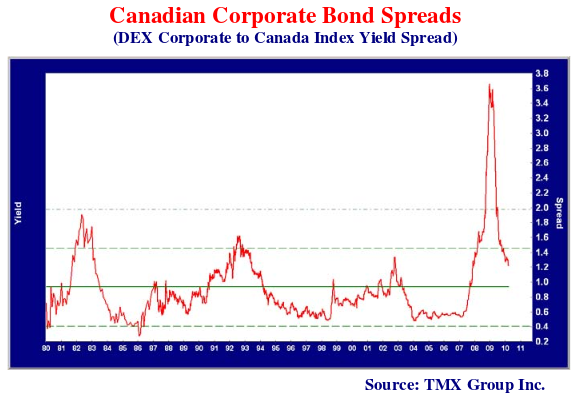

As the chart above shows, we are well above the average corporate bond spread of .93% since 1980. We are also nowhere near the absolute tight of .28% in 1986. The yield spread was .49% in 1997, when we inauspiciously started Canso to specialize in corporate bonds and was again matched in 2004. It is not happenstance that the cyclical tight in yield spreads occurs just before the monetary cycle changes from loosening to tightening. Valuations suggest there is still good value in the corporate bond market. We think the force of the recent rally augurs for a similar correction on the downside once interest rates are sufficiently raised. Until then, the historically wide yield spreads on corporate bonds argue for them.